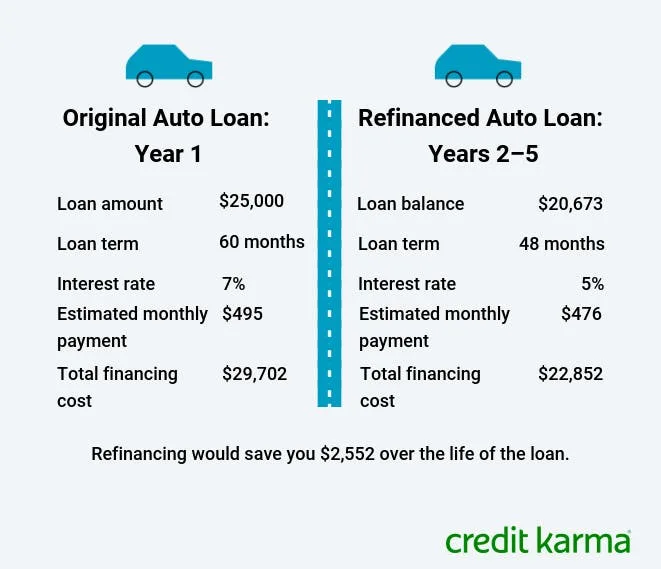

How Long Is Car Finance?

Car finance usually lasts 36 to 72 months, but many buyers now choose terms as long as 84 months to lower the monthly payment.

The simple answer is this: the best car finance term is usually 48 to 60 months if you can afford the payment. A longer loan can make the monthly payment look easier, but it usually means paying more interest and staying in debt longer. Edmunds recommends a 60-month auto loan if you can manage it.

Common Car Finance Terms

Most car loans are offered in these lengths:

36 months: Higher payment, less interest, faster payoff.

48 months: Strong balance if the vehicle price is reasonable.

60 months: Common and usually the best practical term for many buyers.

72 months: Lower payment, but more interest and more risk of negative equity.

84 months: Lowest payment, but usually the riskiest option.

The Consumer Financial Protection Bureau explains that the loan term is the length of the auto loan, usually expressed in months. A shorter term usually means higher monthly payments, while a longer term can lower the payment but increase the total cost.

What Is the Average Car Loan Length?

Car loans have gotten longer because vehicle prices and monthly payments have gone up.

Bankrate reports that the average new-car loan term was about 68.94 months in Q4 2025, while the average used-car loan term was about 67.68 months, based on Experian data.

That means many buyers are financing cars for close to six years. It may be common, but that does not automatically make it smart.

Is 72-Month Car Finance Bad?

A 72-month car loan is not always bad, but it is risky.

It can help lower the monthly payment, which may make sense if you need reliable transportation and cannot afford a shorter term. But the downside is that you pay interest for longer and may owe more than the car is worth for part of the loan.

That is called negative equity. It becomes a problem if you want to trade in the vehicle early, sell it, or if the car is totaled in an accident.

Is 84-Month Car Finance Worth It?

Usually, 84-month car finance should be avoided unless there is a strong reason.

Seven years is a long time to pay for a vehicle. By the end of the loan, the car may need tires, brakes, repairs, maintenance, and possibly major service while you are still making payments.

A long loan is especially risky on used cars because the vehicle may already have mileage and age before the loan even starts.

New Car vs Used Car Finance Length

New cars can often qualify for longer finance terms because they are newer, lower-risk collateral for lenders.

Used cars usually have shorter financing limits, especially if they are older or higher mileage. In Canada, Ratehub notes that new-car loans can stretch up to 96 months, while used-car loans are often shorter because lenders may limit financing based on vehicle age.

For used vehicles, the loan should ideally not outlast the useful life of the car. Financing an older car for six or seven years can become expensive if repairs start before the loan is paid off.

Best Car Finance Term

For most buyers, the best car finance term is:

48 months if you want to pay it off faster.

60 months if you want the best balance.

72 months only if the payment is still comfortable and the interest rate is reasonable.

84 months only if you fully understand the long-term cost.

A good rule: if you need 84 months to afford the payment, the car may be too expensive.

Final Answer

Car finance is usually 36 to 72 months, with 60 months being the best practical target for many buyers.

A longer term lowers the monthly payment, but it increases total interest and keeps you in debt longer. The smartest move is to choose the shortest loan you can comfortably afford while still leaving room for insurance, fuel, maintenance, repairs, and savings.

Connect with us