Buying a car in California is not just about the sticker price.

Whether you are buying a new car, buying a used car, purchasing from a California dealership, or bringing in a vehicle from another state like Texas, you need to understand taxes, title transfer fees, registration costs, smog rules, and DMV paperwork.

The short answer is this: California buyers usually pay sales or use tax, title fees, registration fees, and a Vehicle License Fee based on the vehicle’s value. The exact amount depends on the vehicle price, where the vehicle will be registered, whether it is new or used, and whether it was bought from a dealer or private seller.

If you are shopping for a new or used vehicle in Southern California, it is smart to compare the total out-the-door price before signing. You can start by browsing available new inventory or used inventory and then factoring in taxes, title, registration, and financing.

How Much Is California New Car Tax?

California vehicle tax is usually based on where the vehicle will be registered, not just where you buy it.

The California DMV says use tax on a dealer-purchased vehicle can range from 7.25% to 10.25%, depending on the new registered owner’s city and county of residence. The DMV also notes that title transfer fees may apply when registering a vehicle purchased from a dealer. (California DMV)

That means a buyer in one California city may pay a different total tax rate than a buyer in another city. For example, a car buyer in Los Angeles County may not have the same exact combined tax rate as a buyer in Ventura County, Riverside County, or San Diego County.

This is why “California new car tax” is not one flat number for every buyer. The statewide base is only part of the equation. Local district taxes can change the final rate.

New Car Sales Tax in California: How It Works

When you buy a new car from a licensed California dealer, the dealer generally collects the applicable sales or use tax as part of the transaction.

The tax is calculated on the taxable selling price of the vehicle. That usually includes the agreed purchase price, but the exact taxable amount can depend on rebates, incentives, trade-ins, and how the deal is structured.

For shoppers, the easiest way to think about it is simple:

The more expensive the vehicle, the higher the tax amount.

The city and county where the vehicle is registered affect the rate.

Dealer documentation, registration, title, and DMV fees are separate from the vehicle price.

A $40,000 vehicle taxed at 7.25% would create a lower tax bill than the same vehicle taxed at 10.25%. That difference can matter when you are budgeting your total purchase cost.

California Tax on New Cars vs Used Cars

California tax rules apply to both new and used vehicles.

If you buy from a California dealer, the dealer usually handles the tax collection and DMV processing. If you buy from a private seller, you may need to pay applicable use tax and transfer fees directly through the DMV when transferring title and registering the vehicle.

The California Department of Tax and Fee Administration explains that California sales tax generally applies to vehicles purchased from registered dealers in California, while use tax applies to vehicles purchased from private parties or outside California for use in the state. (CDTFA)

So whether you are buying a new car in California or buying a used car in California, you should expect taxes and DMV fees to be part of the final cost.

How Much Are Title and Registration Fees in California?

California title and registration fees vary by vehicle.

There is no single universal number that applies to every buyer because DMV fees can include several pieces. California DMV lists registration-related charges such as registration fees, title transfer fees, county/district fees, and the Vehicle License Fee. The DMV states that the Vehicle License Fee, or VLF, is 0.65% of the purchase price or vehicle value for most vehicles. (California DMV)

That means a more expensive vehicle typically carries a higher VLF.

California registration costs may include:

Registration fee.

Title transfer fee.

Vehicle License Fee.

Use tax.

County or district fees.

Weight fees for some vehicles.

Smog transfer fee when applicable.

Special plate or lienholder-related fees when applicable.

Because these fees depend on the vehicle and location, California DMV provides an official fee calculator for new vehicles, used vehicles, renewal fees, and new resident vehicles. (California DMV)

DMV Title Transfer Fee Calculator: What to Use

If you are trying to estimate “how much is title registration and other fees,” the safest source is the California DMV’s own calculator.

The DMV calculator includes options for:

Registration renewal fees.

New vehicles purchased from a California licensed dealer.

Used vehicles purchased in California.

New resident vehicles previously registered outside California.

That is useful because a buyer purchasing a new Ram 1500 from a dealer has a different fee situation than someone buying a used Jeep Wrangler from a private seller or bringing a vehicle in from Texas.

A third-party tax title calculator can help you estimate, but the DMV calculator is the official place to start.

Buying a New Car in California: What You Need

If you are buying a new car from a California dealer, the process is usually easier than a private-party purchase.

A licensed dealer will typically handle much of the DMV paperwork, tax collection, registration submission, and temporary operating documents. That is one of the advantages of buying from a dealership instead of trying to manage every title and registration step yourself.

Before buying, you should have:

A valid driver’s license.

Proof of insurance.

Financing approval or payment method.

Trade-in documents, if applicable.

Current registration and title for your trade-in.

Your correct address for tax and registration.

The DMV advises buyers to understand their rights, compare vehicle prices and interest rates, read the purchase contract carefully, and understand warranties and optional products before signing. California dealers must also show buyers a National Motor Vehicle Title Information System report. (California DMV)

If you are preparing to buy, you can also complete a finance application before visiting the store so you have a clearer idea of payment options.

Buying a Used Car in California

Buying a used car in California involves many of the same tax and registration considerations as buying a new car, but there are a few extra things to check.

Used buyers should pay attention to:

Vehicle history.

Title status.

Mileage.

Smog certification.

Open recalls.

Prior damage.

Lien status.

Registration status.

Fees due.

If you buy from a licensed California dealer, the dealer handles many of these steps. If you buy from a private seller, you need to be more careful because you are responsible for making sure the title transfer, tax, fees, smog paperwork, and registration are handled correctly.

The DMV says that for private-party purchases, buyers have 10 days after purchasing a vehicle to transfer ownership, while sellers have 5 days after the sale to report the transfer. (California DMV)

That 10-day window matters. Missing deadlines can create penalties or registration problems.

Buying a Used Vehicle in California From a Private Seller

If you are buying a used car from a private seller, do not hand over money until you verify the paperwork.

You should confirm:

The seller’s name matches the title.

The VIN on the car matches the title.

The odometer disclosure is complete if required.

The title is not branded in a way you did not expect.

There is no lien unless properly released.

The seller provides smog certification when required.

The bill of sale is complete.

The DMV says any change in ownership or lienholder must be reported within 10 days, and the title must be updated. (California DMV)

A private-party deal may look cheaper up front, but mistakes can cost time and money later. If the title is missing, the smog certificate is not valid, or the registration has unpaid fees, the buyer may inherit a headache.

California Smog Rules When Buying a Car

Smog rules are one of the most important parts of buying a used car in California.

California DMV says that if someone sells a car, they generally need to give the new owner a valid smog certification when the vehicle is sold. (California DMV)

The Bureau of Automotive Repair says vehicles that are four model years and newer do not need a Smog Check for change of ownership; instead, California law requires a smog transfer fee due to DMV. (Bureau of Automotive Repair)

This matters because a used car that cannot pass smog may be difficult or impossible to register normally in California. If you are buying privately, do not assume you can “just smog it later.” Get the requirement handled before money changes hands.

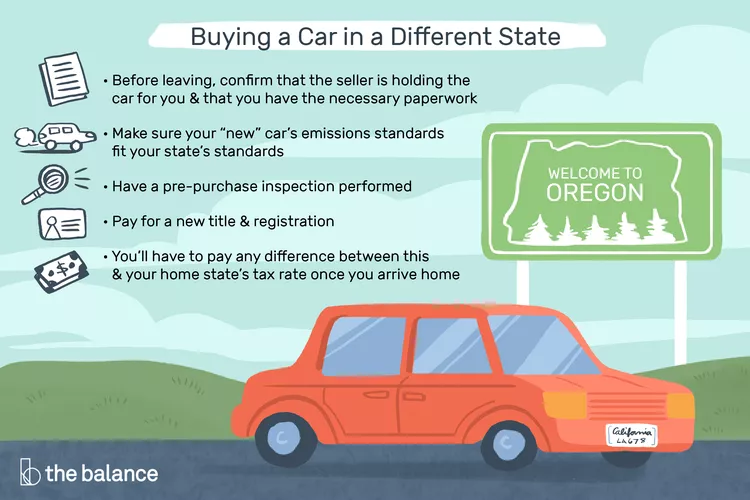

Buying a Car Out of State and Bringing It to California

Buying a car out of state for use in California can work, but it is not a shortcut around California taxes or registration rules.

If you buy a vehicle outside California and bring it into the state for California use, California use tax may apply. CDTFA explains that use tax applies to vehicles purchased from outside California for use in the state, and the purchaser is generally responsible for reporting and paying it if the seller did not collect California tax. (CDTFA)

That means buying a new car from Texas to California, Nevada to California, Arizona to California, or Oregon to California does not automatically eliminate California tax. If the vehicle will be registered and used in California, expect California tax and registration rules to matter.

Buying a New Car From Texas to California

If you buy a new car from Texas and bring it to California, the main questions are:

Can the vehicle be registered in California?

Does it meet California emissions requirements?

Was tax already collected by the selling dealer?

Will California use tax still be owed?

What title and registration paperwork is needed?

Will a smog inspection or vehicle verification be required?

California DMV says out-of-state vehicles must meet California requirements, including emission-control requirements, and DMV cannot register a vehicle if it does not qualify. (California DMV)

This is especially important for new or nearly new vehicles. Not every out-of-state vehicle is automatically California-ready. Before buying, confirm the emissions label and California compliance status.

New California Resident Vehicle Registration

If you move to California with a vehicle that was previously registered in another state, you need to register it in California.

California DMV says that if you bring a vehicle into California that was previously registered in another state or country, you must register it within 20 days of becoming a resident or bringing the vehicle into the state. (California DMV)

This is different from buying a California vehicle from a dealer. New residents may need forms, inspections, fees, and proof of ownership. DMV’s new resident vehicle calculator can help estimate costs.

What Is TTL on a Car?

TTL usually means tax, title, and license.

In car buying, TTL refers to the government-related costs that are added to the price of the vehicle. Depending on the state and transaction, TTL may include sales tax, use tax, title transfer fee, registration, license plates, county fees, and other required charges.

In California, shoppers often use terms like:

TTL car.

Tax title calculator.

Title tax calculator.

Tax title and tag calculator.

Tax and tag calculator.

Tax title and registration fees.

The exact phrase changes, but the question is the same: “What will I actually pay beyond the vehicle price?”

The answer is that California buyers should calculate the out-the-door price, not just the advertised price.

How to Estimate Tax, Title, and Registration in California

To estimate California tax, title, and registration, use this basic approach:

Start with the vehicle selling price.

Add applicable sales or use tax based on the registration address.

Add DMV title and registration fees.

Add the Vehicle License Fee.

Add any county, district, weight, or plate-related fees.

Add dealer documentation and optional products only if applicable.

Subtract trade-in value, rebates, or down payment only where they legally apply to the final deal structure.

Then confirm the estimate with the dealer or DMV calculator.

The most reliable estimator is the official DMV fee calculator because California fees can vary based on location, vehicle type, value, and transaction type. (California DMV)

California Car Buyer’s Bill of Rights

California has specific consumer protections for car buyers.

The California DMV explains that the Car Buyer’s Bill of Rights affects retail vehicle sales by requiring California-licensed dealers to provide an itemized price list for financial items such as warranties and insurance, and to provide buyers with their credit score and an explanation of how it is used. (California DMV)

The California Department of Justice also says the Car Buyer’s Bill of Rights gives buyers certain protections when buying a new or used vehicle from a licensed California dealer, including buyer disclosures. (California DOJ Attorney General)

For used car buyers, California law also includes rules around a contract cancellation option in certain dealer transactions. The Los Angeles County Department of Consumer and Business Affairs explains that the Car Buyer’s Bill of Rights affects new and used car purchases from licensed dealers, and that used car buyers may be able to purchase a two-day sales contract cancellation option. (LACDBA)

New Car Purchase vs Used Car Purchase in California

A new car purchase usually gives you:

Manufacturer warranty.

Dealer-handled DMV paperwork.

Known vehicle history.

Current emissions compliance.

Newest safety and technology features.

A used car purchase may offer:

Lower purchase price.

Slower depreciation.

More choices by budget.

Potentially lower insurance costs.

But used buyers need to inspect more carefully. The lower purchase price may not be worth it if the vehicle has title problems, deferred maintenance, accident history, emissions issues, or unpaid registration fees.

For buyers comparing both options, check new vehicles and used vehicles side by side. The best deal is not always the cheapest price. It is the best total cost with the least risk.

What Do You Need to Buy a Car in California?

To buy a car in California, you typically need:

A valid driver’s license or accepted identification.

Proof of insurance.

A payment method or financing approval.

Proof of income if financing.

Proof of residence if required by lender.

Trade-in title or payoff details if trading a vehicle.

Co-buyer information if applying jointly.

For cash purchases, the paperwork may be simpler. For financed purchases, the lender may require additional documents before approval.

If you are not sure what payment you qualify for, starting with a finance application can make the buying process smoother. You can review financing through the dealership’s credit application.

Can You Avoid California Car Tax by Buying Out of State?

Usually, no.

If the vehicle is purchased for use in California, California use tax may apply even if the vehicle was bought somewhere else. CDTFA states that use tax applies to vehicles purchased from outside California for use in the state. (CDTFA)

Trying to avoid California tax by improperly registering a vehicle out of state can create legal and financial problems. If you live in California and use the vehicle in California, you should follow California registration and tax rules.

How Long Do You Have to Transfer a Title in California?

For private-party purchases, the buyer generally has 10 days to transfer ownership, and the seller has 5 days to report the sale to DMV. (California DMV)

For title changes more generally, DMV says any change in ownership or lienholder must be reported within 10 days. (California DMV)

If you are buying from a dealer, the dealer usually processes the paperwork. If you are buying privately, you need to make sure the transfer happens quickly.

Why Out-the-Door Price Matters

The out-the-door price is the number that matters most.

It includes the vehicle price plus taxes, title, registration, government fees, dealer fees, and any optional products you choose.

A low advertised price may not mean much if the final out-the-door number is much higher. Before agreeing to any deal, ask for a clear written breakdown.

Your buyer’s order should show:

Selling price.

Taxes.

Title and registration.

Dealer fees.

Optional products.

Trade-in allowance.

Payoff amount.

Rebates or incentives.

Down payment.

Total amount financed.

Monthly payment if financing.

This is the cleanest way to compare offers from different dealers.

FAQs About Buying a Car in California

How much is California tax on a new car?

California DMV says use tax on a vehicle purchased from a dealer can range from 7.25% to 10.25%, depending on the registered owner’s city and county of residence. (California DMV)

How much are title and registration fees in California?

Title and registration fees vary by vehicle, value, location, and transaction type. California DMV lists the Vehicle License Fee at 0.65% of the purchase price or vehicle value for most vehicles. (California DMV)

Is there a California DMV title transfer fee calculator?

Yes. California DMV provides an official fee calculator for registration renewal, new vehicles, used vehicles, and new resident vehicles. (California DMV)

Do I pay tax when buying a used car in California?

Yes, tax usually applies to used car purchases in California. Dealer sales generally involve sales tax collection, while private-party or out-of-state purchases may involve use tax. (CDTFA)

Can I buy a car in Texas and register it in California?

Yes, but the vehicle must meet California registration and emissions requirements, and California use tax may apply if the vehicle is brought into California for use in the state. (California DMV)

How long do I have to transfer a car title in California?

For private-party purchases, California DMV says buyers have 10 days after purchase to transfer ownership, and sellers have 5 days to report the sale. (California DMV)

Do I need a smog check when buying a used car in California?

Often, yes. California DMV says sellers generally need to give the buyer a valid smog certification when selling a car, though some newer vehicles may instead require a smog transfer fee. (California DMV)

What is TTL when buying a car?

TTL means tax, title, and license. In California, this can include sales or use tax, title fees, registration fees, Vehicle License Fee, county or district fees, and other required DMV charges.

Final Thoughts: Know the Full Cost Before Buying a Car in California

Buying a car in California is easier when you understand the full cost before signing.

The price on the window sticker or online listing is only one part of the deal. California buyers also need to account for sales or use tax, title transfer, registration, Vehicle License Fee, smog rules, and any required DMV paperwork.

If you are buying from a licensed dealer, much of the paperwork is handled for you. If you are buying privately or bringing in a vehicle from another state, you need to be more careful with title, emissions, taxes, and deadlines.

The smartest move is to compare the out-the-door price, check the DMV fee calculator, understand your buyer rights, and choose a vehicle that fits your budget after all taxes and fees are included. For local shoppers, start with current new inventory, compare available used cars, and review financing options before making your final decision.

Connect with us